Top 8 Digital Health Trends in Technology

Healthcare's digital transformation is happening before our eyes. Digitization has already reshaped industries like consumer goods, automotive and banking, and healthcare is actively following suit. Digital technology and cloud connectivity are now "must have" enhancements for many medical devices and other products within healthcare.

Historically, the pace of technological advancement in healthcare has been slower than other industries, due in large part to the combination of safety and quality concerns layered against complex regulatory requirements. While the pandemic did test every assumption, system and solution in the healthcare industry, it also helped to fast-track trends that have been primed and ready for more extensive rollout for the last few years.

Adoption of emerging platform-based solutions, like telemedicine, was accelerated by as much as three to four years. Remote patient monitoring products have likewise been much in the news and will continue to be a valuable tool for improving care access and efficacy of treatment. Acceptance is broadening across key players in the healthcare ecosystem, including payers, providers and, of course, patients.

Shifts in the delivery of treatment models are being driven by digital healthcare technology that closes the gap between patient and provider, facilitating more in-home care and self-driven care. Traditionally reactive medical response is giving way to a more proactive pursuit of wellness. When considered in light of the extraordinary costs of healthcare, this trend towards precision medicine or personalized healthcare is exactly what the doctor ordered.

Emerging capabilities like artificial intelligence (AI), machine learning and next-generation sequencing (NGS) technologies are delivering new and powerful ways to provide more cost-effective treatment of illness and disease. Advanced surgical instruments and implants, diagnostic tools, pharmaceutical delivery solutions and digital health platforms are transforming the industry. Investment in innovation and next-gen capabilities is ramping too. The global digital health market is booming, projected to hit around $551 billion by 2027, with an expected CAGR of almost 16.5%, according to Precedence Research.

What is Digital Health?

Connected medical devices generate a continuous stream of health data purposed for patient support, predicting or preventing poor outcomes and otherwise curating perspective to help overcome some of our biggest modern health concerns.

Chronic health conditions take an enormous toll on quality of life. Studies estimate that approximately 45% of all Americans suffer from at least one chronic disease, and these numbers are increasing with an aging population — not just in the U.S., but around the world.

One way to frame the big picture: The demand for efficient, cost-effective healthcare delivery is growing exponentially, yet there are concerning bottlenecks on the supply side of the equation. Adequately trained healthcare workers are overworked, stressed, and there's simply not enough of them. Meanwhile, costs across the healthcare system continue to rise squeezing patients, payers and providers alike.

The market is rewarding those who can deliver healthy outcomes, driving adoption of digital health innovations.

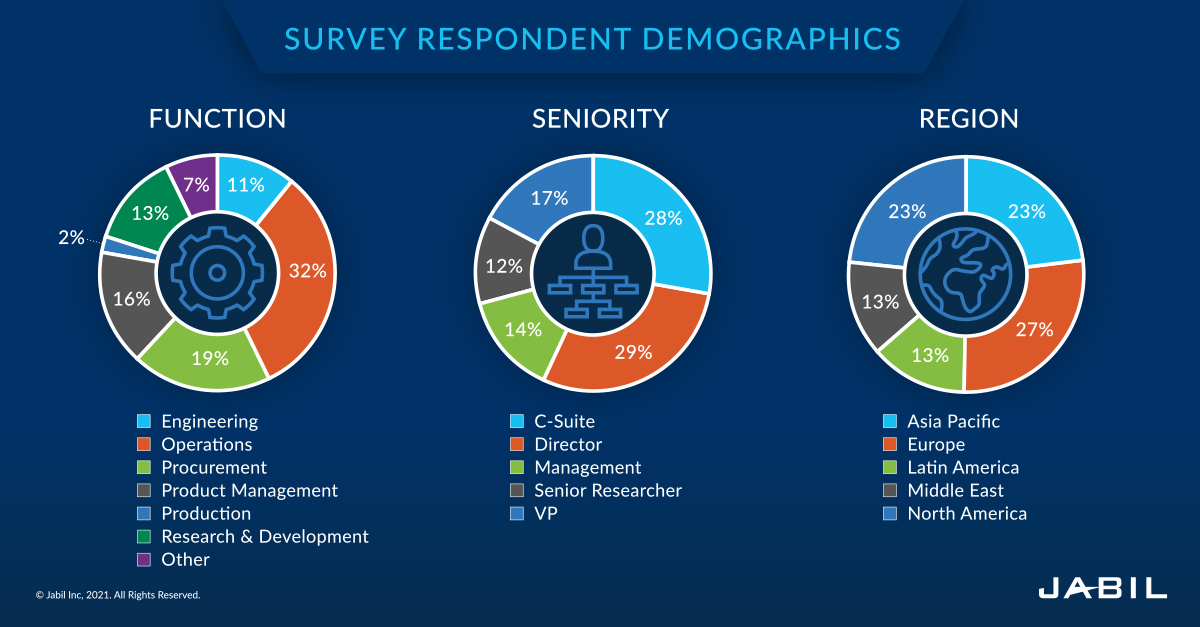

To gain insight into both the adoption and development process, Jabil Healthcare partnered with SIS Research International to conduct a survey of 210 individuals with decision-making responsibility at leading healthcare companies with existing or planned digital healthcare solutions.

Download Jabil’s 2021 Digital Healthcare Technology Trends report.

While the participant base has shifted over the years, this year's survey features a significantly more diverse group across regions, allowing us to make geographical comparisons.

Many of the individuals and companies we surveyed are involved in developing Internet of Medical Things (IoMT) devices, so it aligns with our finding that connected, patient-focused health devices are the digital solutions most commonly in development or production by our respondents.

Half of participants said they are developing or planning solutions focused on patient monitoring, addressing concerns like falls and heart rate, while 43% are developing diagnostic solutions like MRIs or ultrasounds. The market for on-body and wearable devices, which 41% of respondents are developing, is hotter than ever. Global sales of the devices, including smart watches and fitness trackers, was up 32% in Q2 of 2021 compared with Q2 of 2020 according to the analyst firm IDC.

As the number of solutions in development and the consumer demand for them rise in tandem, it's clear that there has been significant progress in the digital health space since our first survey in 2018. While challenges certainly remain in the development and adoption of digital health solutions, the future is bright and holds tremendous opportunities. Here are the top eight digital health technology trends:

1. Digital Health Technology is Almost Ready for Prime Time

Tools like wearables and smartphone health apps help consumers take control of their own wellness and have easy to access information they can discuss with their medical providers right at their fingertips. Similarly, new connected digital health devices can help relieve the stress that can come with simply following doctor's orders.

Digital devices like auto-injectors or smart inhalers can not only deliver the exact amount of medication you need, but it can also send that information to connected apps or platforms and keep your provider in a real-time adherence and compliance loop for assessing efficacy of treatment. Connected health technology is transforming the way clinical trials are conducted within the pharmaceutical industry precisely because of this quantifiable and actionable two-way facilitation of communication, helping to ensure the most effective and efficient testing of a study's hypothesis by clinical trial administrators.

Healthcare companies are moving ever closer to bringing digital solutions of increasing complexity like these to the masses. More than half of companies surveyed are at least in the development stage with their digital solutions, with 28% of them in the testing phase.

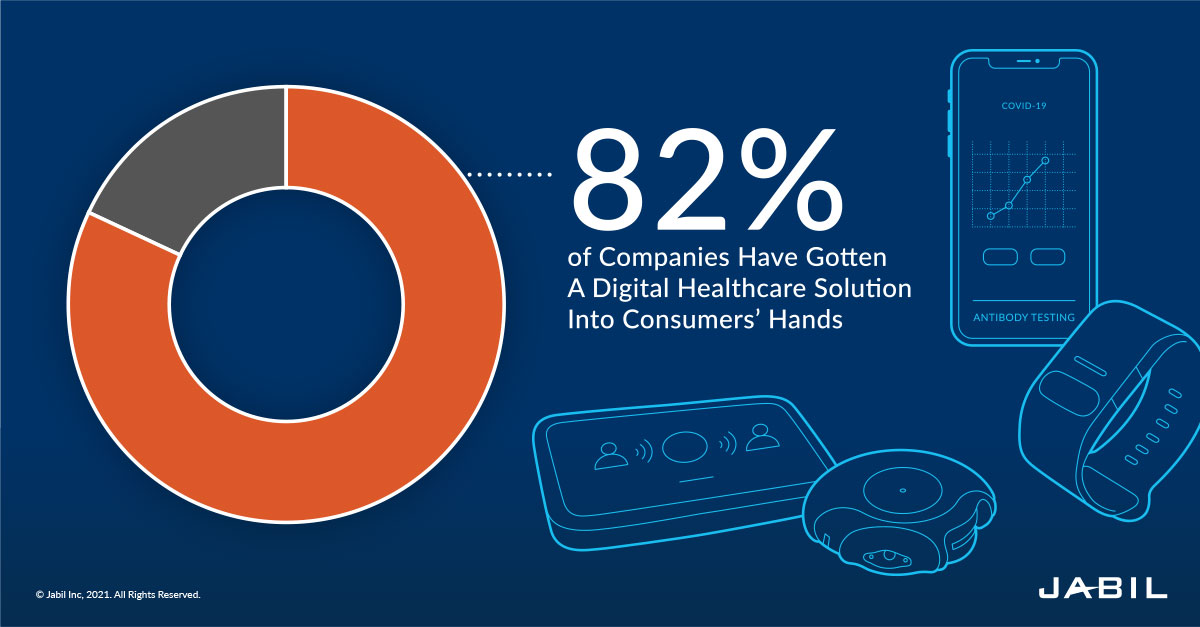

Promisingly, consumers and providers are already having the opportunity to benefit from the new levels of care these solutions can offer. Our survey found that 82% of companies have gotten some type of digital healthcare solution into the hands of consumers, mostly for clinical trials or testing (32%) or for use by a select group (32%). Close to a fifth of respondents reported fully launching their solution to their users.

2. Regulatory Processes & Underlying Technology Needs Are Major Digital Health Challenges

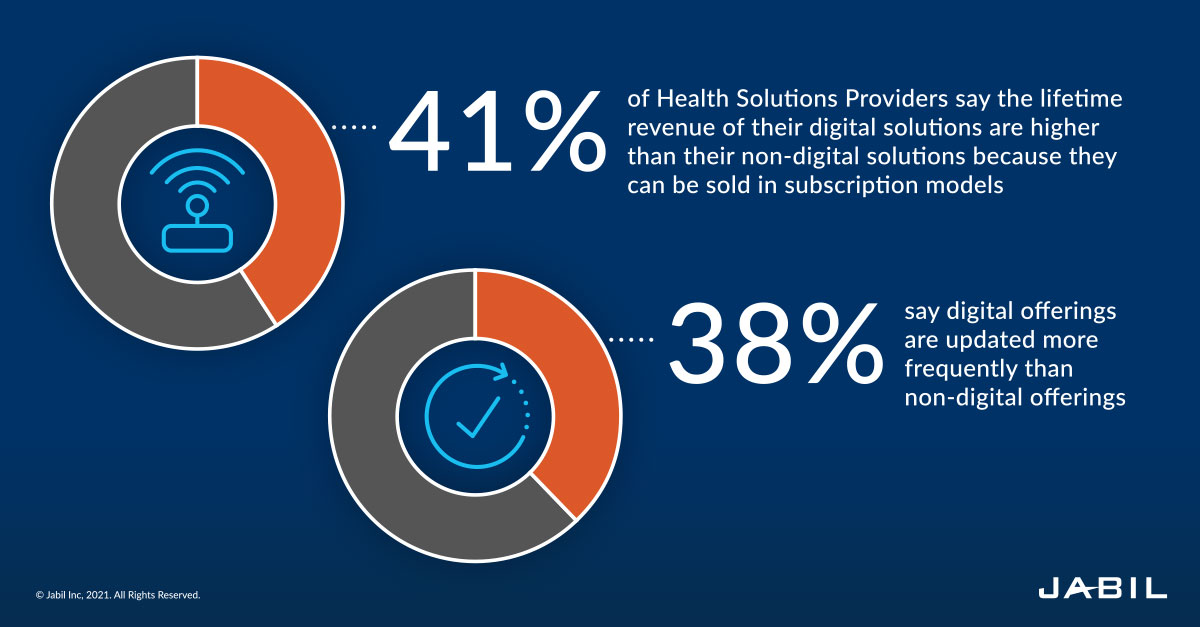

For medical device companies, digital solutions bring several advantages over traditional devices. First, 41% of companies said the lifetime revenue of their digital solutions are higher than their non-digital solutions because they can be sold in a subscription model.

The market has a number of intriguing wellness and fitness tracking products that collect, measure and analyze biometrics from blood oxygen saturation to sleep cycles. The device, often a wristband, is typically connected to an app that provides analytics, training guides and coaching paid for via a monthly subscription fee.

That means revenue coming in every month; not just when a new generation of the band technology drops. And 38% of survey respondents did indeed say their digital offerings are updated more frequently than their non-digital offerings thanks to software updates that can be sent out with the push of a button. With digital solutions, as long as the core therapy doesn't change, the surrounding technologies can be updated as often as needed — meaning the device, system or software doesn't need to go through the regulatory process again.

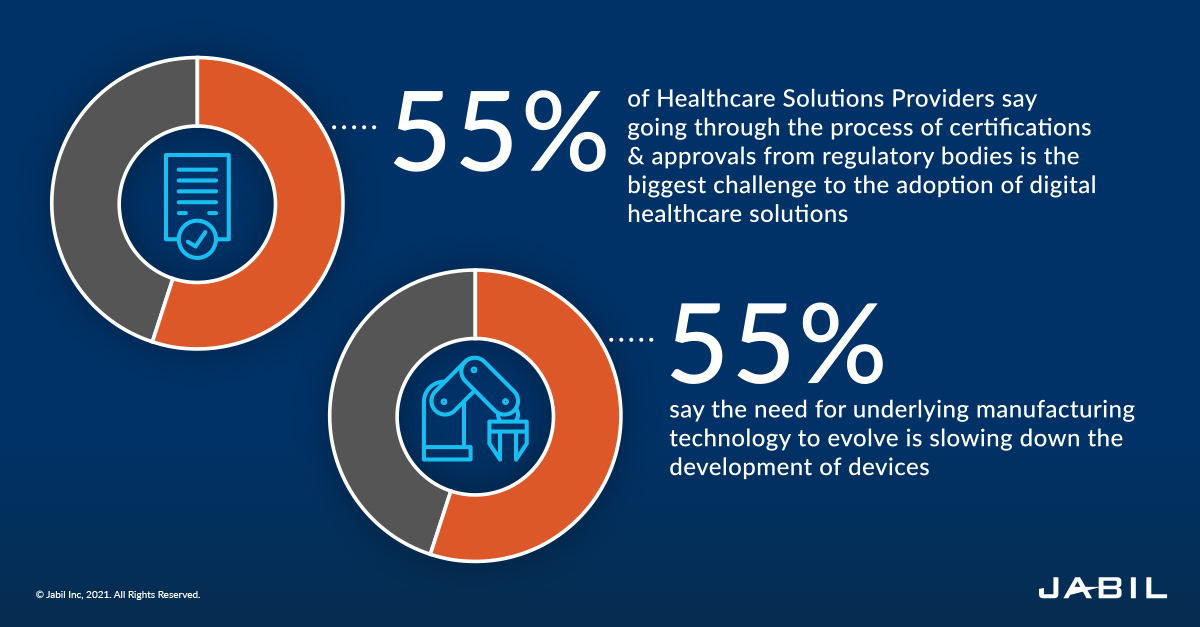

Going through this process of certifications and approvals from regulatory bodies is the biggest challenge to the adoption of digital healthcare solutions, 55% of survey respondents say. Delays are longest for devices that go inside patients' bodies, such as pacemakers, and infection detection devices. In North America, however, half of the companies surveyed said payment responsibility and reimbursement was an adoption hurdle.

The last few years have seen dramatic support from the FDA for addressing the accelerative nature at the heart of digital healthcare. Programs such as their Breakthrough Devices Program and the Digital Health Software Precertification (Pre-Cert) Program help speed up development, assessment and review. Likewise, the issuance of recent rulings amending the definition of a device in the Federal Food, Drug, and Cosmetic Act (FD&C Act) to exclude certain software functions is more affirmation that fast-paced innovation will be fostered in tandem with securing standards.

The agency is also turning to technology like AI to better incorporate real-world data into its regulatory decisions, like information from electronic health records, wearables and physicians treating patients, instead of relying solely on clinical trial results.

However, regulations and certifications are not the only slowdown for digital health solutions on their way to market. In manufacturing digital health solutions, the exact same percentage of companies (55%) say that the need for the underlying manufacturing technology to evolve is slowing down the development of devices. Finally, component shortages, which are in turn driving up manufacturing costs, are also slowing down development.

3. Consumer Demand is Pushing for Faster Digital Healthcare Product Development Cycles

Nine in 10 survey respondents said consumer demand is increasingly pushing for innovation in digital healthcare devices, bringing the time-to-market closer to that of consumer electronics. Accordingly, 92% said healthcare companies need to act more like consumer technology companies and deliver solutions more quickly.

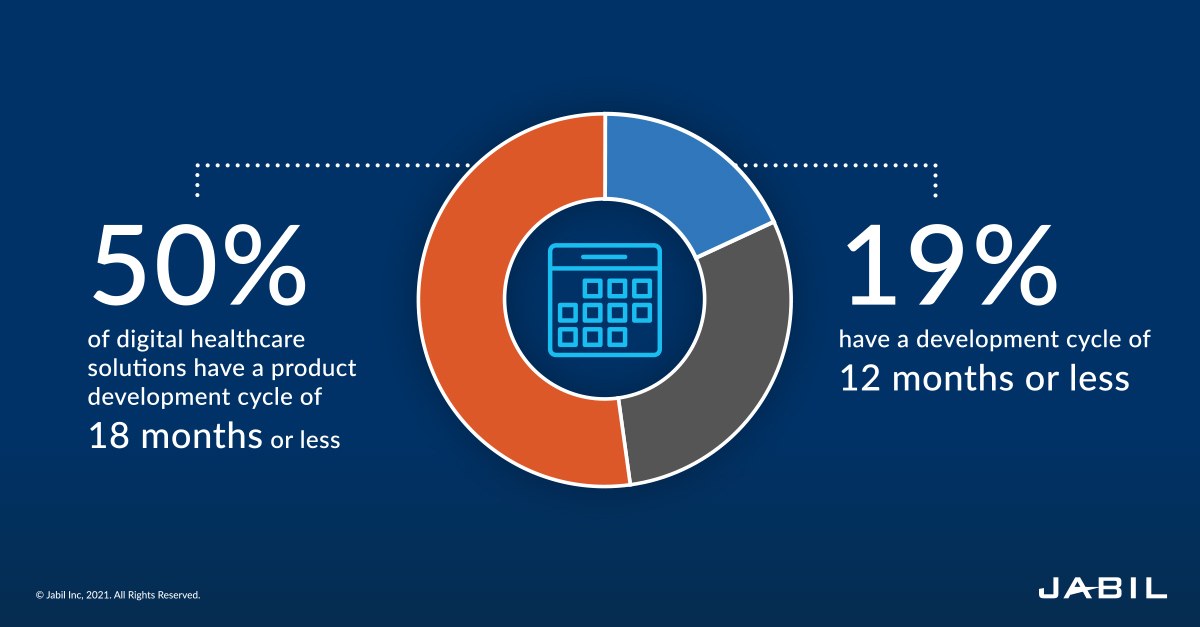

They're certainly on the right track. Exactly half of survey respondents now have a product development cycle of 18 months or less, up from 41% in our 2020 survey. About a fifth (19%) say their digital healthcare solutions development cycle is even shorter — 12 months or less. Almost no digital solutions take longer than 36 months to develop, highlighting the vast difference between these devices and systems and pharmaceuticals, which typically take years to develop.

The positives are many for digital healthcare solutions. However, half of respondents agreed that digital healthcare solutions are often frustrating for consumers — from difficulties connecting devices to Wi-Fi to getting apps and hardware to "talk" with one another. More than nine in 10 respondents said digital healthcare should be standardized to enable interoperability between devices and within product platforms from various brands.

The objective of data interoperability within healthcare is to build an improved system that will allow users to find, understand and act on information when they need it, regardless of the dataset. True, seamless data interoperability requires a spirit of collectivism in which data becomes democratized. Recent regulations from the Office of the National Coordinator for Health IT (ONC) and the Centers for Medicare and Medicaid Services (CMS) are certainly a nudge in the right direction, enabling more widespread sharing of health information by healthcare providers and health plans to improve treatment, care coordination and public health.

Once the digital health solutions are developed, tested and approved, it's not always smooth sailing, though. Consumers are pushing for innovation in digital healthcare, but they're also setting up some roadblocks for healthcare companies.

4. Consumer Data & Privacy Concerns Come to Healthcare

By now you've heard debates and discussions surrounding the data privacy of IoT devices; for consumers and manufacturers alike, these concerns extend to IoMT devices.

A 2021 Accenture survey on consumer adoption of digital health found that 30% of respondents would be more likely to use digital technology to manage their health if they had more confidence in data security and privacy. Overall, Accenture found, the rise of virtual healthcare during the COVID-19 pandemic has made more people think about their data rights; almost three-quarters of respondents (73%) said they are now considering that they should have the right to approve the collection and usage of their personal health information for any purposes beyond treatment.

As such, 43% of companies in our survey said they have concerns about consumer adoption of digital healthcare solutions, with half or more of North American and European companies reporting those concerns. In those two regions, there is a particular concern around privacy, security and consumer data. The devices that collect the most patient data — wearables, in-body and patient-monitoring devices — ranked the highest for consumer adoption concerns.

Companies believe consumers might be hesitant to give them that much constant access to personal health information. In response, healthcare companies need to change how they operate to put the proper team in place to support the needs of their new digital health solutions — including data privacy.

5. Healthcare Solution Providers are Making Organizational Changes That Support Digital Transformation

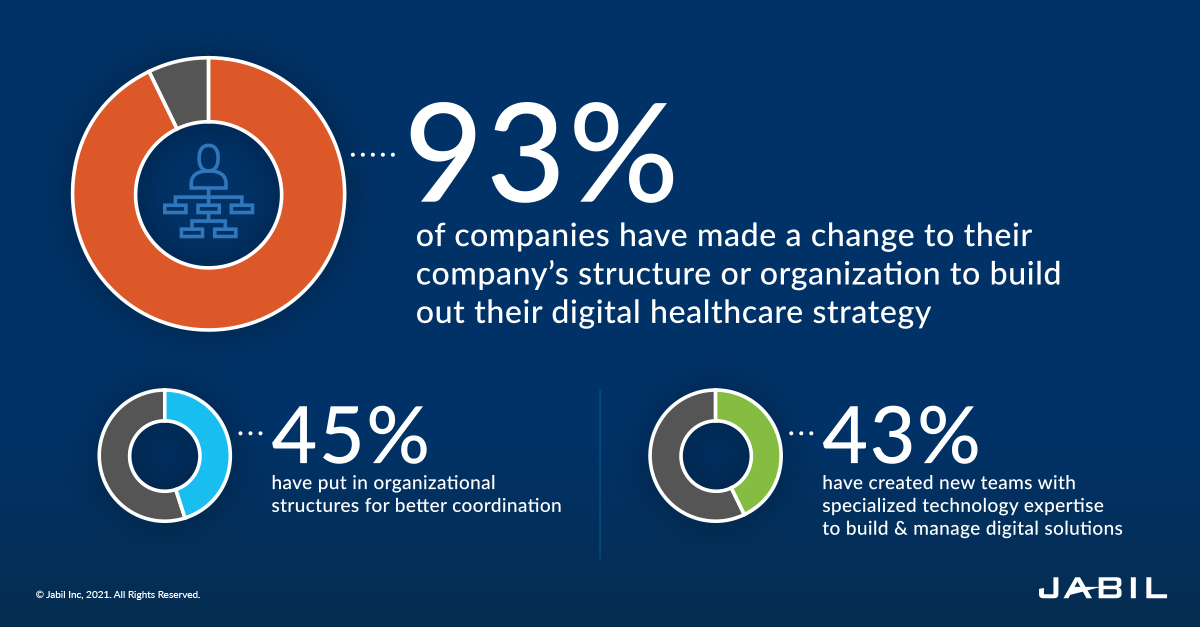

For healthcare companies, big changes to their product offerings have come with changes to the way their organization is structured to support this new marriage of health and tech. The overwhelming majority, 93%, of companies surveyed made some sort of change to the way their organization's structure or operation to build out their digital healthcare strategy. In North America, almost half (47%) of companies chose not to change their organizational structure, possibly due to a more mature industry in the region.

There are different approaches to making the organizational changes necessary in support of launching digital solutions. About 45% have put in organizational structures, like hybrid reporting or a digital tiger team of subject matter experts, to ensure better coordination. A similar number, 43%, have created new teams with expertise in fields like big data or software user interface for the hands-on work of building and maintaining their solutions. The organizational changes depend on the solution being developed.

About a third of companies agreed that collaboration is key, saying that they partner with other companies to fill organizational gaps or hire consultants to explore new options. Building a collaborative culture that keeps the focus on your "why" allows for more agility throughout the organization and is less siloed from one department to another. Impediments will be knocked down, and innovation will start happening in new and exciting ways.

6. Business Models Focus on the Patient

Healthcare isn't just about taking care of people who are already sick. It's about keeping people healthy and preventing illness and injury in the first place. By monitoring patients when they're in good health, providers — and patients — can catch early signs of disease when they're more treatable.

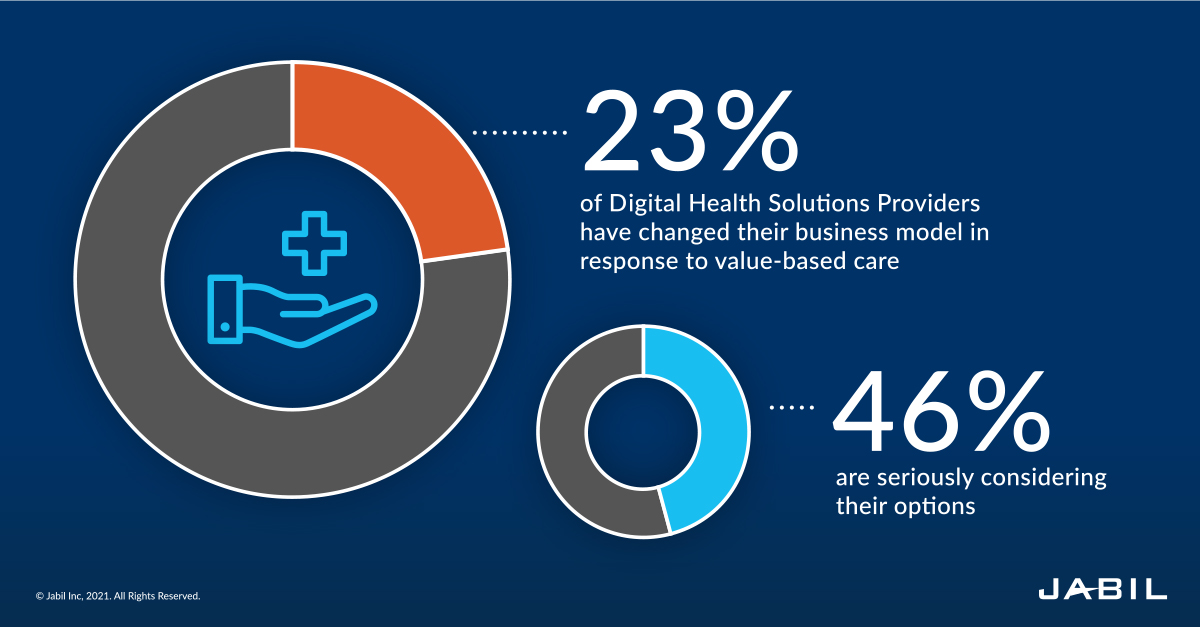

That's the idea behind the value-based care model (VBC). A major reason for the adoption of digital health solutions, many of which focus on patient monitoring and tracking, is to help practitioners and healthcare systems make a concerted push toward embracing this model in all aspects of their care. About a quarter, 23%, of healthcare companies surveyed have already changed their business model in response to the industry-wide shift to VBC, while 46% are seriously considering their options.

Companies across the globe and across the healthcare sector and sub-industries are also focused on personalized healthcare - 77% of survey respondents are seriously considering options or already creating personalized solutions. The top solution here is 3D printing, with 60% of companies who produce those types of solutions seriously considering their options. Additive manufacturing in healthcare can be a game-changer particularly in orthopedics. Up to 27% of hip surgery re-revisions are due to poor fixation and biomechanical reconstruction of the initial implant. Personalized, patient-specific implants manufactured with today's additive manufacturing technology are dramatically improving revision rates, reducing hospital and post-acute care costs and generating consistently higher marks in patient satisfaction.

While the data provided by digital healthcare solutions gives patients and providers new insights into health and wellness, it also gives companies new options for revenue streams. Our survey found that 63% of companies are considering options, with fewer companies in Asia, Europe and North America giving it thought due to consumer data and privacy laws like HIPAA. What patients want, or don't want, is ultimately driving the future of digital health.

7. Medical Device OEMs are Turning to External Partners for Digital Health Solutions

Enlisting outside expertise is one of the most effective ways to solve challenges within your solution ecosystem. Partners help identify market trends, which can determine product lifecycles and potential redesigns. Encouraging collaboration with industries outside your own is a vital strategy for navigating inevitable change and disruption. Few respondents said they would not need any external help, indicating that healthcare companies have recognized that partners can help manage risk, solve challenges and provide expertise that is not traditionally found in the health space.

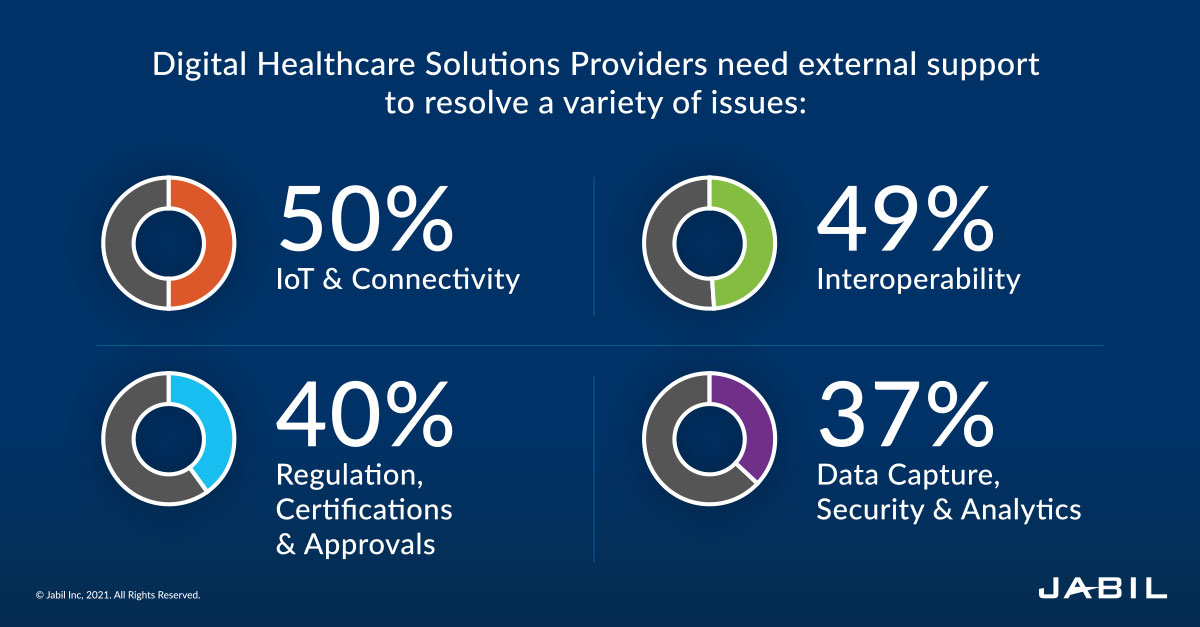

About half of respondents said IoT and connectivity issues, plus interoperability, are the top concerns they'll need support from partners to resolve. Then, 40% and 37% of companies, respectively, said challenges with regulation, certifications and approvals as well as data capture, security and analytics will require outside expertise. The technological capabilities manufacturing partners bring to the table will help companies deliver healthcare solutions, 63% of respondents said.

Healthcare is another industry now facing shortages of chips, semiconductors and other electronic components necessary for digital health solutions. Partners who are well versed in these supply chains can assist healthcare companies overcome these new and unprecedented challenges as they enter the IoT space. Half of survey respondents said manufacturing partners could help navigate changing technology, supplier and regulation landscapes.

Another important capability OEMs should engage is sustaining engineering — the technical support of a product from the time it moves into manufacturing until the product is retired. It's a way to harness future momentum downstream in a product's lifecycle to best ensure its relevance will be optimized in a crowded and competitive field of challengers.

Part of the competition intensity in this landscape is being driven by the entrance of new players, including big tech, into the digital healthcare space. Despite this focus on technology, our survey found that healthcare-first companies are still leading the way.

8. Technology Companies Create Urgency, But Healthcare Manufacturers Drive the Industry

It's no secret that technology companies from Google to Amazon to Apple have disrupted industries from retail to news to, yes, healthcare. In 2021, Google launched a pilot program of Care Studio, its electronic health record (EHR) software that organizes patient records and allows practitioners to, in essence, perform a Google search on a patient's record to quickly and easily find what they need.

With a recent operating system update, Apple gave iPhone and Apple Watch users the option to securely share medical data with family, medical providers or caretakers, while Amazon has gotten deeper into healthcare with the expected expansion of telehealth and in-person services through Amazon Care. All three tech companies have strategically expanded their capabilities by acquiring healthcare companies, from Fitbit (Google) to Health Navigator (Amazon).

These initiatives send a powerful message to the rest of the industry to speed up their product development cycle to align with the pace of technology that consumers have come to expect. The convergence of "big tech" and healthcare will allow for technology-driven solutions that will power precision medicine.

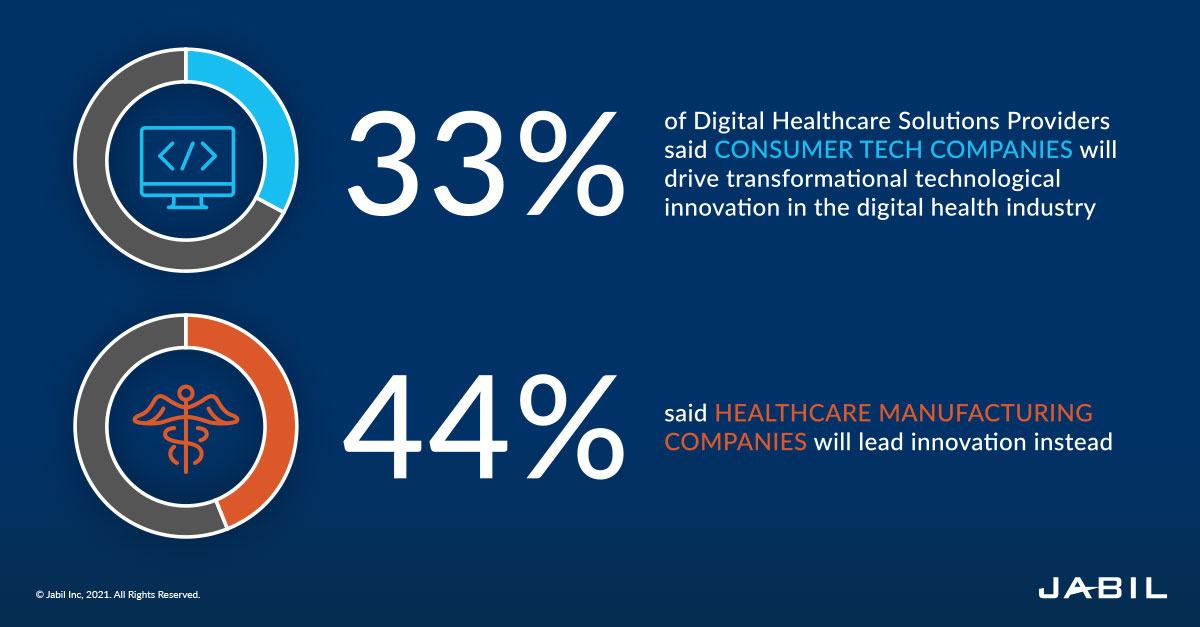

One-third of survey respondents say these consumer tech companies will drive transformational technological innovation in the digital health industry. The consumer tech industry rated particularly highly for its leadership in wearables and patient monitoring (fall monitoring, heart rate monitoring) — areas where we have seen consumers embracing smart watches and health tracking apps built into their smartphones. Still, a solid 44% of survey respondents say healthcare manufacturing companies that understand certification and production will lead the charge on innovation.

Collaboration between all of these players will transform the way healthcare is delivered. The next generation of digital health solutions will likely depend on partnerships between healthcare, technology and manufacturing companies.

The digital health market has blossomed in recent years, yet there's still so much more room for growth. Artificial intelligence, 5G's dramatic latency reduction and overall upgrade on the infrastructure of wireless connectivity, and the adoption of wearables and other emerging technologies are all truly going to deliver a digital revolution right before our eyes. It's coming along and picking up speed. Our destination (for now) is VBC.

Given the top digital health trends we discussed above, what are you doing to embrace these opportunities and position yourself for the ones coming next?

Download the 2021 Digital Health Tech Trends Survey Report

Insights from over 200 digital health decision-makers on the barriers, opportunities and the future of digital health.